Renters’ insurance, also referred to as tenant insurance, plays an important role in providing financial protection to members of the renting population, but a common misconception is keeping many of them from taking out coverage.

Insurance Business digs deeper into this form of coverage in this part of our client education series. We will discuss what renters’ insurance covers and what it doesn’t, explain the reason behind the coverage gap, and give practical tips on how tenants can make the best out of their policies.

Insurance industry professionals can share this article with their clients to help them understand the real value this type of coverage offers.

Taking out renters’ insurance is not legally required, although landlords often make it a condition of the rental agreement – and for good reason. Tenant insurance can go a long way in helping renters protect themselves and personal belongings when accidents and disasters strike.

For rental properties, it is the owner’s responsibility to obtain protection for the building and its fixtures and fittings. This type of coverage – also known as landlord insurance – however, does not include the tenants’ possessions. For them to be protected, they must purchase a separate renters’ policy.

Renters’ insurance works the same way as contents coverage in a standard homeowners’ policy. It covers a tenant’s possessions, including clothing, furniture, personal electronics, and appliances. High-priced jewelry – such as wedding bands and engagement rings – expensive artwork, and other high-value items may likewise be covered by purchasing a rider.

There are two ways in which renters are paid under a tenant insurance policy:

Replacement value: Covers the full cost of replacing lost or damaged possessions with brand-new versions.

Actual cash value: Also called ACV, this reimburses what the item was worth at the time of the loss or damage.

According to many industry experts, renters’ insurance is among the cheapest and easiest type of coverage customers can obtain, making it generally a smart investment.

Standard tenant insurance policies typically include three core coverages, according to the Insurance Information Institute (Triple-I). These are:

This covers personal items, including the following:

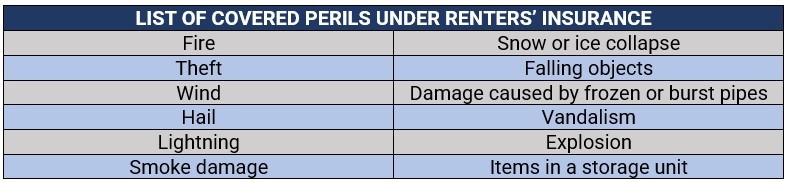

Most renters’ insurance plans provide coverage for loss or damage caused by the perils listed in the table below.

Some policies also cover belongings lost or damaged while outside the rental property, like a bicycle or a laptop, for example. Others impose limits on valuable possessions such as jewelry and art collections, although full coverage through a rider can be purchased separately.

Tenant insurance provides two types of liability coverage:

Also called ALE, this pays for living expenses incurred if the tenant needs alternative accommodation due to the rental property becoming uninhabitable. Coverage typically includes the following, subject to limits:

Apart from these standard inclusions, renters can customize their policies with endorsements that add more coverage but often at an extra cost. These include:

Just like other policies, renters’ insurance has exclusions. Here are some items that are not included in this type of coverage.

Tenant insurance offers contents, liability, and ALE coverage for certain types of water damage. These include those caused by the following:

Renters’ insurance will only cover water damage if this was not due to negligence or intentionally caused, and if the policyholder did what was needed to prevent it. Coverage likewise does not extend to subletted or subleased units. In the case of toilet overflow, most policies provide cover as long as it is a one-time event.

There are five major factors that impact premium prices of a renters’ insurance policy. These are:

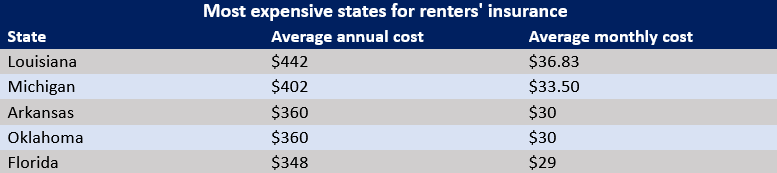

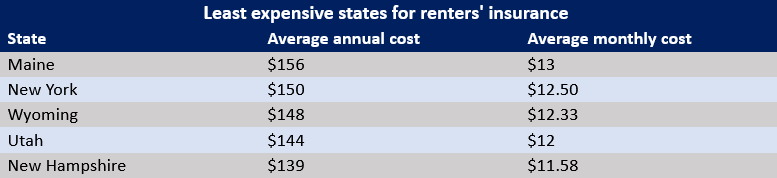

Renters' insurance is one of the least expensive forms of coverage, but the premiums still vary depending on the region.

The average tenant insurance premiums in the US cost $179 annually or about $15 monthly, according to Nationwide. Rates can be higher or lower depending on the state. The table below lists the top five states where premiums cost the most and the least, according to the data.

You can view the profiles of America’s best renters’ insurance providers in our ongoing Special Reports features.

Several factors affect the cost of a tenant insurance policy in Canada, including the following:

Standard premiums range between $15 and more than $40 per month or $300 and $480 annually, based on the calculations of several price comparison websites Insurance Business reviewed.

Check out the list of Canada’s best insurance companies in our ongoing Special Reports features.

The UK’s renting population can take out contents-only coverage of a home insurance policy, which cost between £59 and £66 annually, according to research done by us at Insurance Business. This works out at about £4 to £5.50 monthly. Given the low cost, tenant insurance is worth having unless a person’s possessions are really limited.

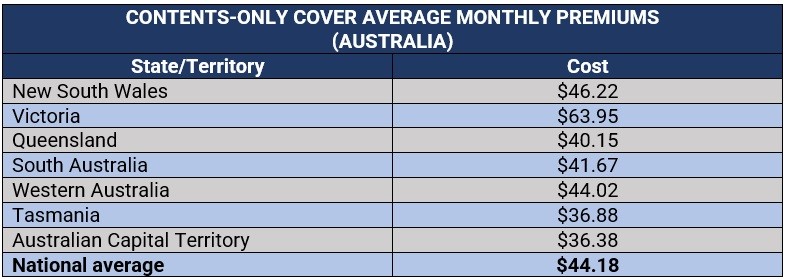

In Australia, renters’ insurance – also called renters’ contents insurance – and contents-only cover offer basically the same protection. The main difference is that some tenant insurance policies provide coverage for accidental damage to any fixtures or fittings in the rental home – dented walls or doors, for example.

Some insurers also offer cheaper renters’ insurance policies designed to cover only loss or damage due to fire and theft. Tenants can take out a home contents insurance policy, but they must make sure that the coverage provided is adequate and fits their budget. The table below shows how much contents-only cover costs for belongings worth $100,000 in different states and territories.

Although renters’ insurance is already among the cheapest forms of coverage, insurers still give discounts to tenants, allowing them to slash insurance premiums further. Here are some ways renters can access tenant insurance discounts:

One of the most common misconceptions that keep tenants from taking out renters’ coverage is that their personal belongings are protected under their landlord’s insurance. In reality, however, this kind of policy covers the structure of the property and the contents the landlord owns within the premises such as furniture and appliances. It is up to the tenant then to take out coverage for their personal possessions.

Others skip coverage because they feel it is unnecessary as their belongings may not be worth as much. However, even the cost of small items can add up quickly if they need to be replaced all at once. For these reasons, renters’ insurance can be a smart investment, especially with accidents and disasters often occurring without warning.

What about you? Is renters’ insurance something you feel is worth purchasing? Are there other benefits or drawbacks of this type of coverage that you want to share? Feel free to use our comment box below.